When it comes to borrowing money, one of the biggest decisions you’ll face is choosing between fixed and variable rates. Which one will save you money?

Which one offers peace of mind? Your choice could impact your monthly payments, your financial stability, and how much interest you end up paying over time. Understanding the key differences between fixed and variable rates is essential to making a smart decision that fits your unique situation.

Ready to find out which option is right for you? Keep reading, and you’ll learn everything you need to know to make confident, money-wise choices.

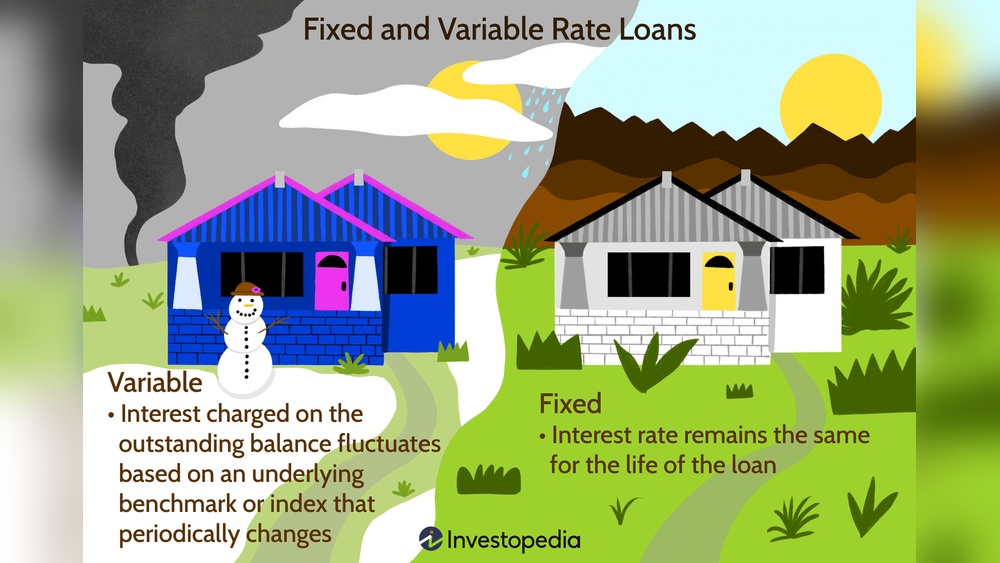

Fixed Rates

Fixed rates mean your interest stays the same for the loan term. This gives you consistent monthly payments. You know exactly how much to pay every month. It helps with budgeting and planning your finances.

One big benefit is stability. Your payments never change, even if market rates rise. This protects you from surprises. Another benefit is easy to understand and compare. You avoid the stress of fluctuating costs.

Drawbacks include usually starting with a higher interest rate than variable rates. This can mean paying more in interest overall. You also miss out on savings if market rates fall. Fixed rates lack flexibility if rates drop.

Variable Rates

Variable rates change over time. They are tied to a benchmark or index. This means your interest rate can go up or down at set periods.

One big benefit is the usually lower starting rate. This can save money if rates stay low or drop. Payments might be smaller at first.

Another benefit is the chance to pay less interest if market rates fall. Some loans have smaller penalties for paying off early.

Drawbacks include unpredictable payments. If rates rise, monthly costs can go up fast. This can make budgeting hard.

Risk is higher with variable rates. You could pay much more over time. Also, some lenders can increase rates quickly, adding stress.

Comparing Fixed And Variable Rates

Fixed rates keep your payment the same every month. This means you know exactly how much to pay. It helps a lot with budgeting because there are no surprises. You won’t be affected by interest rate fluctuations. Your payment stays stable even if the market changes. But fixed rates may start higher than variable ones.

Variable rates can change over time. They are tied to market rates and can go up or down. This means your payment might be lower at first but could increase later. It can be harder to predict monthly payments. This adds some risk because your budget may need adjusting. Variable rates might save money if rates fall, but cost more if rates rise.

| Fixed Rate | Variable Rate | |

|---|---|---|

| Payment Predictability | Payments stay the same every month. | Payments can change with market rates. |

| Interest Rate Fluctuations | Not affected by market changes. | Changes with the financial benchmark. |

| Impact on Budgeting | Easier to plan monthly expenses. | Harder to predict future costs. |

| Risk Factors | Low risk, stable payments. | Higher risk, payments can rise. |

:max_bytes(150000):strip_icc()/dotdash-mortgage-rates-fixed-versus-adjustable-rate-Final-19297b62a75d4263b9865092467f306d.jpg)

Choosing The Right Rate

Assessing your financial goals helps decide between fixed or variable rates. Fixed rates keep your payments stable. This is good for budgeting and long-term plans. Variable rates may start lower but can change. They can save money if interest rates drop.

Loan term considerations matter too. Fixed rates suit long loans for steady costs. Variable rates might work for short loans if you expect rates to stay low. Think about how long you want to borrow money.

Market conditions affect which rate is better. If rates are low and expected to rise, fixed rates protect you. When rates are high but may fall, variable rates might save money.

Personal risk tolerance is key. Fixed rates give peace of mind. Variable rates carry more risk but can be cheaper. Choose what feels safe for your budget and comfort level.

Fixed Vs Variable In Different Loans

Mortgages with fixed rates keep payments the same each month. This helps with easy budgeting and less surprise costs. Variable rates can start lower but may rise if market rates go up. This can make monthly bills change and sometimes become higher.

Student Loans often offer fixed or variable rates. Fixed rates stay steady, so payments don’t change. Variable rates may be lower at first but can increase, affecting your monthly budget and total cost.

Personal Loans usually have fixed rates, giving clear payment plans. Variable rates are less common but could save money if interest rates fall. Risk of payment rises is higher with variable rates.

Auto Loans mostly use fixed rates. This means steady payments and no surprises. Variable rates might start low but could increase, making it harder to predict monthly costs.

Strategies For Smart Borrowing

Locking in fixed rates is smart when you want steady payments. Fixed rates protect from rising interest costs. They work best if you plan to keep your loan long. Budgeting is easier with fixed rates because payments stay the same. This helps avoid surprises in your monthly bills.

Variable rates can be useful when interest rates are low or expected to drop. They usually start with a lower rate than fixed loans. Payments may go down if market rates fall. But they can also rise, causing payment shocks. Variable rates suit borrowers who can handle some risk.

Refinancing lets you switch between fixed and variable rates. It can save money if rates change. Check fees and penalties before refinancing. Some loans charge for early payoff.

Managing payment changes means planning your budget carefully. Track market interest trends if you have a variable rate. Stay ready for higher payments. Use savings or extra income to cover increases. This keeps your borrowing smart and stress-free.

Common Mistakes To Avoid

Ignoring rate changes can lead to unexpected costs. Fixed rates stay the same, but variable rates can rise or fall. Missing these shifts might hurt your budget.

Overlooking fees and penalties is another big mistake. Some loans charge for early repayment or rate switching. Always check for hidden costs before choosing.

Underestimating budget impact is risky. Variable rates might start low but can climb, increasing monthly payments. Fixed rates offer steady, easy-to-plan costs.

Failing to shop around limits your options. Different lenders offer varying rates and terms. Comparing offers helps find the best fit for your needs.

Resources And Tools

Loan comparison guides help you understand fixed and variable rates. These guides show the pros and cons clearly. They help you see which rate fits your needs best.

Interest rate calculators let you enter loan amounts and terms. You get monthly payment estimates instantly. This tool helps compare different loan options easily.

Financial advising services provide expert advice. They explain how rates affect your budget and loan costs. Speaking with an advisor can clarify your choices.

Market trend updates keep you informed about current interest rates. This information shows if rates are rising or falling. Staying updated helps in planning your loan timing.

Frequently Asked Questions

Is It Better To Have A Fixed Or Variable Rate?

Choosing fixed rates ensures stable, predictable payments, ideal for long-term budgeting. Variable rates may start lower and save money if interest drops but carry payment risks. Select based on your risk tolerance and financial goals.

How To Get A 4% Interest Rate On A Mortgage?

Secure a 4% mortgage interest rate by maintaining excellent credit, making a large down payment, and choosing a fixed-rate loan from reputable lenders. Shop around, compare offers, and consider locking rates early during low-interest market periods.

Is 4.75 A Good Interest Rate?

A 4. 75% interest rate is generally good, especially in a low-rate environment. It offers predictable payments and long-term stability. Compare it with current market rates and loan types to ensure it fits your financial goals.

Is It Better To Get A Variable Rate Or Fixed Rate Loan?

Fixed-rate loans offer stable payments and budgeting ease. Variable rates start lower and may save money if interest rates drop but carry payment risks. Choose based on your risk tolerance and financial goals.

Conclusion

Choosing between fixed and variable rates depends on your needs. Fixed rates keep payments steady and help with budgeting. Variable rates start lower but can change, which means risk and reward. Consider how long you will borrow and your comfort with payment changes.

Understanding both types helps you make a smart choice. Take your time and review your options carefully. This way, you can find a rate that fits your financial goals.