Looking for the best mortgage deal can feel overwhelming. You want to make sure you’re not paying more than you should over the life of your loan.

That’s where a Mortgage APR Comparison Report becomes your secret weapon. By comparing Annual Percentage Rates (APR) from different lenders side by side, you get a clear picture of the true cost of your mortgage—not just the interest rate, but all the fees and charges rolled in.

This means you can confidently choose the mortgage that saves you the most money and fits your financial goals. Keep reading to discover how to use a Mortgage APR Comparison Report to take control of your home loan and make smarter, more informed decisions. Your wallet will thank you.

:max_bytes(150000):strip_icc()/Annual_Percentage_Rate-0c5e018f6e1148a29c55c0a356c2a411.png)

Mortgage Apr Basics

APR stands for Annual Percentage Rate. It shows the true cost of a mortgage loan. Interest rate only shows the cost of borrowing money. APR includes extra fees and costs too. This makes APR a better tool for comparing loans.

People should pay attention to APR. It helps to understand how much money will be paid over time. Loans with the same interest rate can have very different APRs. The loan with the lower APR usually costs less overall.

| Component | Description |

|---|---|

| Interest Rate | The percentage charged on the loan amount annually. |

| Loan Origination Fees | Fees paid to the lender for processing the loan. |

| Discount Points | Optional fees paid to lower the interest rate. |

| Mortgage Insurance | Insurance required if the down payment is low. |

| Other Fees | Costs like appraisal and credit report fees. |

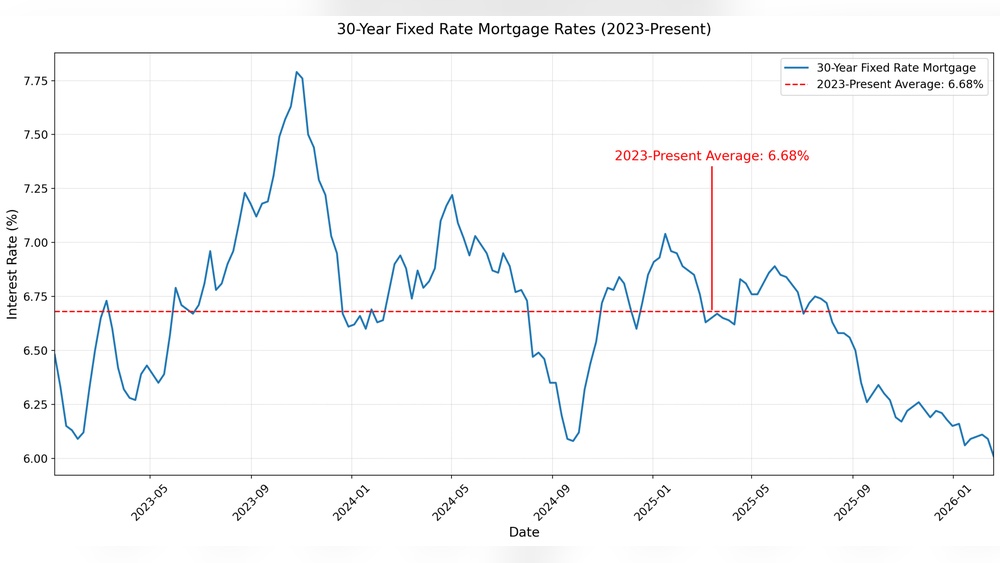

Current Mortgage Apr Trends

Today’s average APR rates for mortgages generally range between 6% and 7%. These rates can change daily due to market shifts. Fixed-rate mortgages keep the same APR during the loan term, while adjustable-rate mortgages may change after an initial period. Lenders use your credit score, loan size, and down payment to set your APR.

Factors influencing APR include credit history, loan type, and economic conditions. A higher credit score usually means a lower APR. Larger down payments can also reduce your APR. Economic changes like inflation or Federal Reserve actions impact all mortgage APRs.

| Region | Average APR Range | Notes |

|---|---|---|

| South | 5.8% – 6.5% | Lower rates due to local market competition |

| Midwest | 6.0% – 6.7% | Stable rates with moderate variation |

| West | 6.2% – 7.0% | Higher rates linked to housing demand |

| East | 6.1% – 6.8% | Rates vary with urban vs rural areas |

Tools For Comparing Aprs

Online comparison calculators help you check different mortgage APRs quickly. Enter loan amount, term, and credit score to get results. These tools show monthly payments and total costs side by side. They save time and reduce guesswork.

Rate charts list APRs from various lenders. Use them to spot trends and find the lowest rates. Focus on charts updated often to see current offers. They help you understand market changes easily.

Evaluating lender offers means looking beyond just APR. Check fees, loan terms, and payment options too. Ask about prepayment penalties or special deals. Compare all parts of the offer for a clear picture.

Impact Of Credit Score On Apr

The credit score plays a big role in determining your mortgage APR. Higher scores usually mean lower interest rates, which save you money over time. Scores are divided into tiers:

| Credit Score Tier | Typical APR Range |

|---|---|

| Excellent (750+) | 3.0% – 4.0% |

| Good (700-749) | 4.0% – 5.0% |

| Fair (650-699) | 5.0% – 6.5% |

| Poor (below 650) | 6.5% and above |

Raising your credit score can reduce the APR and monthly payments. Simple steps include paying bills on time and lowering debts. Avoid common pitfalls like missing payments, maxing out credit cards, or applying for many loans at once. These actions can hurt your score and increase your mortgage costs.

Down Payment And Apr

Down payment size directly influences your mortgage APR. A larger down payment usually means a lower APR. This happens because lenders see less risk when you invest more money upfront. Small down payments often lead to higher interest rates and extra costs.

Paying at least 20% can help you avoid Private Mortgage Insurance (PMI). PMI adds to your monthly payments and overall loan cost. Some lenders allow smaller down payments but expect to pay PMI until you reach 20% equity.

Consider your savings and budget when choosing a down payment. Balancing a sizable down payment with enough savings for emergencies is key. Larger down payments reduce loan size and monthly payments but may limit your cash reserves.

Comparing Loan Types And Aprs

Fixed-rate mortgages have the same interest rate for the whole loan term. This means monthly payments stay stable. Adjustable-rate mortgages (ARMs) start with a lower rate but can change after a few years. ARMs may save money early but can be risky if rates rise.

Government-backed loans like FHA, VA, and USDA loans often have lower APRs. They help buyers with lower credit scores or smaller down payments. These loans come with special rules and sometimes require mortgage insurance.

| Loan Type | Typical APR Range | Key Features |

|---|---|---|

| Fixed Rate | 3.0% – 5.0% | Stable payments, good for long-term |

| Adjustable Rate | 2.5% – 4.5% (initial) | Lower start rate, can change |

| Government-Backed | 2.75% – 4.25% | Lower credit needs, insurance required |

| Jumbo Loans | 3.5% – 6.0% | For large amounts, higher rates |

Jumbo loans are for amounts above conforming limits. They usually have higher APRs due to more risk. These loans need stronger credit and bigger down payments.

Hidden Costs Affecting Apr

Closing costs and fees can raise the annual percentage rate (APR) on a mortgage. These costs include appraisal fees, title insurance, and inspection charges. They add to the total amount you pay beyond the loan principal and interest.

Loan origination charges are fees lenders charge to process your loan. These fees cover administrative costs and can be a percentage of the loan amount or a flat fee. They directly increase the APR by adding to your upfront expenses.

Both closing costs and origination fees affect your monthly payments and overall loan cost. Always ask for a detailed breakdown of these fees before choosing a mortgage.

Using Apr Comparison To Save Money

Negotiating better rates can lower your mortgage costs significantly. Start by comparing APR offers from different lenders. This helps you spot the best deals. Ask lenders if they can match or beat competitor rates. Sometimes, small changes in your credit score or loan terms can improve your rate. Don’t hesitate to ask for discounts or waivers on fees. Being polite but firm often helps during negotiations.

Locking in your APR means fixing your interest rate at a certain time. This protects you from rising rates before closing. Usually, lenders let you lock rates for 30 to 60 days. Check if there is a fee for locking and if it can be extended. Rate locks offer peace of mind and can save money if rates go up soon after.

Knowing when to refinance is key to saving money over time. Refinance when your new APR is at least 0.5% lower than your current one. Also consider refinancing if you want to change loan terms or tap home equity. Remember to count all costs like closing fees to ensure refinancing actually saves money.

Frequently Asked Questions

What Is A Good Apr For A Mortgage Right Now?

A good mortgage APR right now typically ranges between 6% and 7%, depending on credit score and loan type. Compare multiple lenders for the best rate.

Can A 70 Year Old Woman Get A 30 Year Mortgage?

A 70-year-old woman can get a 30-year mortgage, but approval depends on lender policies and financial health.

What Is The 3 7 3 Rule In Mortgage?

The 3-7-3 rule in mortgage means a lender has 3 days to review your application, 7 days to process, and 3 days to close the loan.

What Salary Do You Need For A $400,000 Mortgage?

You typically need an annual salary of about $100,000 to qualify for a $400,000 mortgage. Lenders prefer your housing costs below 28% of income. This estimate assumes a 30-year loan with a 6% interest rate and 20% down payment.

Conclusion

Comparing mortgage APRs helps you find the best loan for your needs. Small differences in APR can save you thousands over time. Use current data to make smart choices. Check multiple lenders to see who offers the lowest rates. Remember, your credit score and down payment affect your APR.

Keep an eye on market trends for better timing. Taking time to compare APRs leads to smarter home buying. It’s worth the effort to get the best deal possible.